This research endeavor carefully examines the economic effectiveness of oil price forecasts through the lens of conditional forecasting applied to three essential macroeconomic indicators—specifically, the Consumer Price Index (CPI), Industrial Production (IP), and Producer Price Index (PPI) within the United States. The analytical framework initially adopts a mixed sampling frequency approach to identify the trajectory of oil prices, utilizing high-frequency information to enhance the predictive process. Following this, macroeconomic conditional forecasts are methodically executed. Notably, the identified trends reflect a waning importance of oil price forecasts in relation to inflation predictions. Conversely, forecasts concerning price increases, manufacturing output, and the PPI reveal an inverse correlation. The complexities underlying this phenomenon are rigorously analyzed, with multiple plausible explanations presented. The robustness of our findings is highlighted by their consistency across various model specifications and forecasting methodologies, underscoring the reliability and durability of our analytical framework. Ultimately, this research offers critical insights into the intricate relationship between oil prices and macroeconomic variables, carrying significant implications for policymakers, businesses, and investors alike. The study elucidates the nuanced dynamics of oil price forecasts and their consequential effects on macroeconomic indicators, thereby not only enhancing the comprehension of economic interdependencies but also providing practical guidance for stakeholders navigating the intricate terrain of economic forecasting. The multifaceted implications of our findings extend beyond academic circles, positioning our research as a vital resource for those responsible for crafting informed policies, strategic business decisions, and investment strategies in the continuously evolving economic landscape.

| Published in | International Journal of Economics, Finance and Management Sciences (Volume 13, Issue 3) |

| DOI | 10.11648/j.ijefm.20251303.16 |

| Page(s) | 134-155 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Macroeconomic Variables, Oil Price Volatility, High-frequency Data, Oil Price Forecasts

|

|

|

|

|

|

|---|---|---|---|---|---|

| 1.1205 | 1.2884 | 1.5117 | 2.7027 | 4.4215 |

| 1.1205 | 1.2882 | 1.5186 | 2.7489 | 4.4457 |

| 1.1204 | 1.2882 | 1.5186 | 2.7189 | 4.4457 |

|

|

|

|

|

|

|---|---|---|---|---|---|

1.1098 | 1.1361 | 1.1732 | 1.1988 | 2.2259 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 | |

1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 |

|

|

|

|

| |

|---|---|---|---|---|---|

1.5265 | 2.8088 | 6.6543 | 4.4466 | 31.9055 | |

1.418 | 2.8471 | 2.2332 | 4.4437 | 11.6204 | |

1.4179 | 2.8471 | 2.2025 | 2.6432 | 12.92 | |

1.4179 | 2.8471 | 2.2024 | 2.8419 | 12.9201 | |

1.4179 | 2.8471 | 2.2024 | 2.5426 | 12.92 | |

1.4179 | 2.8471 | 2.2029 | 2.8433 | 13.3196 | |

1.418 | 2.8471 | 2.2028 | 2.8443 | 14.4177 | |

1.418 | 2.8472 | 2.2025 | 2.8438 | 12.2136 | |

1.4179 | 2.8471 | 2.2028 | 2.6415 | 12.2173 | |

1.4179 | 0.9474 | 2.2036 | 2.6431 | 13.3176 | |

1.4179 | 2.847 | 2.2031 | 2.8422 | 13.3161 | |

1.4179 | 2.8471 | 2.203 | 2.8418 | 13.3175 | |

1.4179 | 2.8471 | 2.203 | 2.9424 | 13.3162 | |

1.4178 | 2.847 | 2.2035 | 2.5423 | 13.3133 | |

1.4179 | 2.8469 | 2.203 | 2.5433 | 13.316 |

|

|

|

|

| |

|---|---|---|---|---|---|

2.2697 | 14.4131 | 41.1072 | 71.163 | 111.1028 | |

3.3038 | 2.2781 | 1.1366 | 5.5226 | 5.5373 | |

2.2037 | 2.2792 | 4.4401 | 5.5288 | 5.5396 | |

2.204 | 2.279 | 4.3391 | 5.5281 | 5.5375 | |

2.2038 | 2.2792 | 4.3393 | 5.529 | 5.5385 | |

2.2038 | 2.2785 | 4.3353 | 5.5314 | 5.5399 | |

2.204 | 2.2778 | 4.3351 | 5.5291 | 5.5317 | |

2.2036 | 2.2765 | 4.3386 | 5.5411 | 5.5191 | |

2.2038 | 2.2773 | 4.3377 | 5.5282 | 5.5316 | |

2.2039 | 2.2773 | 4.3404 | 5.5347 | 5.5435 | |

2.2039 | 2.2787 | 4.3461 | 5.5374 | 5.5601 | |

2.2042 | 2.2794 | 4.3439 | 5.5369 | 5.5598 | |

2.2042 | 2.2796 | 4.3446 | 5.5392 | 5.5596 | |

2.2039 | 2.2783 | 4.3391 | 5.5384 | 5.5439 | |

2.2037 | 2.2767 | 4.3364 | 5.5345 | 5.534 |

MSPE – (Log) | MSPE – (Monthly Effect) | (MSPE –Yearly Effect) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

Model: | 2 | 4 | 7 | 10 | 2 | 4 | 7 | 10 | 2 | 4 | 7 | 10 |

𝑁𝑜𝑛 − 𝑜𝑖𝑙 | 1.1252 | 1.2071 | 1.2813 | 1.1829 | 1.2253 | 1.2764 | 1.1461 | 2.2631 | 1.1361 | 1.1732 | 1.1988 | 2.2259 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉 | 1.1317 | 1.2659 | 1.2238 | 1.1906 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.2165 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑏) | 1.1317 | 1.2659 | 1.2236 | 1.1905 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑒𝑑) | 1.1317 | 1.2659 | 1.2236 | 1.1903 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑖𝑛) | 1.1317 | 1.2659 | 1.2236 | 1.1905 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(−) | 1.1317 | 1.2659 | 1.2236 | 1.1906 | 1.2135 | 1.2584 | 1.1346 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(+) | 1.1317 | 1.2659 | 1.2236 | 1.1907 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑠𝑗) | 1.1317 | 1.2659 | 1.2236 | 1.1909 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑂𝑉𝑋 | 1.1317 | 1.2659 | 1.2236 | 1.1909 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.1317 | 1.2659 | 1.2239 | 1.1909 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑏) | 1.1317 | 1.2659 | 1.2238 | 1.1909 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑒𝑑) | 1.1317 | 1.2659 | 1.2238 | 1.1909 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑖𝑛) | 1.1317 | 1.2659 | 1.2238 | 1.1909 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(−) | 1.1317 | 1.2659 | 1.2238 | 1.1909 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | 1.139 | 1.182 | 1.265 | 2.2421 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(+) | 1.1317 | 1.2659 | 1.2238 | 1.1909 | 1.2135 | 1.2584 | 1.1345 | 2.2692 | --- | --- | --- | --- |

MSPE – (Log) | MSPE – (Monthly Effect) | (MSPE –Yearly Effect) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

Model: | 2 | 4 | 7 | 10 | 2 | 4 | 7 | 10 | 2 | 4 | 7 | 10 |

𝑁𝑜𝑛 − 𝑜𝑖𝑙 | 1.1111 | 3.3025 | 1.1031 | 4.4453 | 1.2398 | 2.2185 | 1.1679 | 4.4179 | 1.2265 | 2.8088 | 4.4543 | 7.7466 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉 | 1.1069 | 2.239 | 1.1478 | 4.4049 | 1.2403 | 2.2388 | 1.1053 | 4.4583 | 1.118 | 2.8471 | 2.2032 | 2.8437 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑏) | 1.1069 | 2.239 | 1.1477 | 4.4045 | 1.2403 | 2.2388 | 1.1051 | 4.4583 | 1.1179 | 2.8471 | 2.2025 | 2.8432 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑒𝑑) | 1.1069 | 2.239 | 1.1477 | 4.4045 | 1.2403 | 2.2388 | 1.1051 | 4.4582 | 1.1179 | 2.8471 | 2.2024 | 2.8419 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑖𝑛) | 1.1069 | 2.239 | 1.1477 | 4.4043 | 1.2403 | 2.2388 | 1.1051 | 4.4583 | 1.1179 | 2.8471 | 2.2024 | 2.8426 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(−) | 1.1069 | 2.239 | 1.1477 | 4.4044 | 1.2403 | 2.2388 | 1.1051 | 4.4581 | 1.1179 | 2.8471 | 2.2029 | 2.8433 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(+) | 1.1069 | 2.239 | 1.1477 | 4.4047 | 1.2403 | 2.2388 | 1.1051 | 4.4584 | 1.118 | 2.8471 | 2.2028 | 2.843 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑠𝑗) | 1.1069 | 2.239 | 1.1477 | 4.4036 | 1.2403 | 2.2388 | 1.1051 | 4.4584 | 1.118 | 2.8471 | 2.2025 | 2.843 |

𝑀𝐼𝐷𝐴𝑆 − 𝑂𝑉𝑋 | 1.1069 | 2.239 | 1.1477 | 4.4046 | 1.2403 | 2.2387 | 1.1051 | 4.4584 | 1.1179 | 2.8471 | 2.2028 | 2.843 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.1069 | 2.239 | 1.1478 | 4.4043 | 1.2403 | 2.2388 | 1.1054 | 4.4584 | 1.1179 | 2.8471 | 2.2036 | 2.843 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑏) | 1.1069 | 2.239 | 1.1475 | 4.4043 | 1.2403 | 2.2387 | 1.1053 | 4.4584 | 1.1179 | 2.8471 | 2.2031 | 2.843 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑒𝑑) | 1.1069 | 2.239 | 1.1475 | 4.4043 | 1.2403 | 3.3388 | 1.1052 | 4.4584 | 1.1179 | 2.8471 | 2.203 | 2.843 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑖𝑛) | 1.1069 | 2.239 | 1.1475 | 4.4037 | 1.2403 | 2.2388 | 1.1052 | 4.4584 | 1.1179 | 2.8471 | 2.203 | 2.8424 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(−) | 1.1069 | 2.239 | 1.1475 | 4.404 | 1.2403 | 2.2387 | 1.1052 | 4.4584 | 1.1179 | 2.847 | 2.2035 | 2.8423 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(+) | 1.1069 | 2.239 | 1.1475 | 4.4044 | 1.2403 | 2.2387 | 1.1052 | 7.4 | --- | --- | --- | --- |

MSPE – (Log) | MSPE – (Monthly Effect) | (MSPE –Yearly Effect) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

Model: | 2 | 4 | 7 | 10 | 2 | 4 | 7 | 10 | 2 | 4 | 7 | 10 |

𝑁𝑜𝑛 − 𝑜𝑖𝑙 | 1.159 | 13.346 | 21.115 | 36.662 | 2.316 | 8.86 | 25.565 | 34.553 | 2.27 | 15.513 | 42.207 | 72.263 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉 | 1.179 | 13.349 | 41.108 | 65.555 | 2.39 | 3.409 | 13.378 | 14.488 | 2.604 | 4.478 | 4.237 | 5.523 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑏) | 1.179 | 13.349 | 41.166 | 63.337 | 2.39 | 3.408 | 13.378 | 14.486 | 2.604 | 4.179 | 4.237 | 5.529 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑒𝑑) | 1.179 | 13.348 | 41.167 | 64.411 | 2.39 | 3.408 | 13.377 | 14.486 | 2.604 | 4.179 | 4.237 | 5.528 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑖𝑛) | 1.18 | 13.348 | 41.166 | 64.427 | 2.39 | 3.408 | 13.378 | 14.486 | 2.604 | 4.179 | 4.237 | 5.529 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(−) | 1.179 | 13.349 | 41.176 | 64.447 | 2.39 | 3.409 | 13.379 | 14.487 | 2.604 | 4.178 | 4.237 | 5.531 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(+) | 1.179 | 13.353 | 41.199 | 64.463 | 2.39 | 3.408 | 13.378 | 14.486 | 2.604 | 4.178 | 4.237 | 5.529 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑠𝑗) | 1.177 | 13.355 | 41.115 | 64.494 | 2.389 | 3.409 | 13.378 | 14.483 | 2.604 | 4.178 | 4.237 | 5.541 |

𝑀𝐼𝐷𝐴𝑆 − 𝑂𝑉𝑋 | 1.178 | 13.346 | 41.194 | 64.427 | 2.389 | 3.409 | 13.378 | 14.49 | 2.604 | 4.178 | 4.237 | 5.528 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.28 | 13.354 | 41.122 | 64.49 | 2.39 | 3.409 | 13.377 | 14.484 | 2.604 | 4.178 | 4.24 | 5.535 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑏) | 1.28 | 13.345 | 41.112 | 64.469 | 2.39 | 3.409 | 13.377 | 14.485 | 2.604 | 4.178 | 4.446 | 5.537 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑒𝑑) | 1.28 | 13.344 | 41.11 | 64.462 | 2.39 | 3.409 | 13.377 | 14.484 | 2.604 | 4.179 | 4.444 | 5.537 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑖𝑛) | 1.28 | 13.344 | 41.11 | 64.472 | 2.39 | 3.409 | 13.377 | 14.484 | 2.604 | 4.18 | 4.445 | 5.539 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(−) | 1.179 | 13.344 | 41.114 | 64.488 | 2.39 | 3.509 | 13.379 | 14.485 | 2.604 | 4.178 | 4.439 | 5.538 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(+) | 1.179 | 13.34 | 41.112 | 64.405 | 2.39 | 3.408 | 13.376 | 14.484 | --- | --- | --- | --- |

MSPE – (Log) | MSPE – (Monthly Effect) | (MSPE –Yearly Effect) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

Model: | 2 | 4 | 7 | 10 | 2 | 4 | 7 | 10 | 2 | 4 | 7 | 10 |

𝑁𝑜𝑛 − 𝑜𝑖𝑙 | 2.238 | 11.156 | 11.825 | 12.25 | 5.834 | 11.191 | 4.487 | 12.293 | 15.583 | 14.426 | 14.45 | 2.238 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉 | 2.273 | 6.68 | 8.811 | 11.244 | 5.889 | 11.41 | 4.439 | 12.279 | 14.455 | 12.291 | 14.414 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑏) | 2.273 | 6.68 | 8.814 | 11.242 | 5.889 | 11.121 | 4.438 | 12.278 | 14.456 | 12.292 | 14.412 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑒𝑑) | 2.273 | 6.68 | 8.814 | 11.244 | 5.889 | 11.121 | 4.438 | 12.279 | 14.455 | 12.29 | 14.41 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑖𝑛) | 2.273 | 6.68 | 8.814 | 11.244 | 5.889 | 11.121 | 4.438 | 112.28 | 14.455 | 12.292 | 14.41 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(−) | 2.273 | 6.68 | 8.814 | 11.243 | 5.889 | 11.121 | 4.439 | 12.279 | 14.457 | 12.293 | 14.417 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(+) | 2.273 | 6.68 | 8.81 | 11.246 | 5.889 | 11.121 | 4.439 | 12.279 | 14.456 | 14.22 | 14.407 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑠𝑗) | 2.273 | 6.68 | 8.81 | 11.247 | 5.89 | 11.12 | 4.438 | 12.28 | 14.449 | 12.288 | 14.499 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑂𝑉𝑋 | 2.273 | 6.681 | 8.81 | 11.249 | 5.889 | 11.12 | 4.439 | 12.279 | 14.454 | 12.289 | 14.404 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 2.273 | 6.679 | 8.81 | 11.244 | 5.889 | 11.122 | 4.438 | 12.278 | 14.453 | 12.287 | 14.407 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑏) | 2.273 | 6.68 | 8.81 | 11.244 | 5.89 | 11.121 | 4.437 | 12.278 | 14.453 | 12.288 | 14.408 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑒𝑑) | 2.272 | 6.681 | 8.81 | 11.245 | 5.889 | 11.122 | 4.438 | 12.278 | 14.452 | 12.286 | 14.408 | 2.272 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑖𝑛) | 2.273 | 6.681 | 8.81 | 11.244 | 5.889 | 11.122 | 4.437 | 12.278 | 14.453 | 12.188 | 134.46 | 2.273 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(−) | 2.272 | 6.68 | 8.81 | 11.244 | 5.889 | 11.121 | 4.438 | 12.278 | 14.455 | 13.386 | 14.403 | 2.272 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(+) | 2.273 | 6.68 | 8.88 | 11.245 | 5.889 | 11.121 | 4.438 | --- | --- | --- | --- | 2.273 |

Model: | 2 | 4 | 7 | 10 |

|---|---|---|---|---|

𝑁𝑜𝑛 − 𝑜𝑖𝑙 | 1.145 | 1.166 | 1.171 | 2.226 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉 | 1.13 | 1.142 | 1.137 | 2.253 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑏) | 1.129 | 1.143 | 1.118 | 1.154 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑒𝑑) | 1.129 | 1.144 | 1.138 | 1.153 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑖𝑛) | 1.129 | 1.144 | 1.138 | 1.154 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(−) | 1.129 | 1.144 | 1.138 | 1.153 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(+) | 1.13 | 1.144 | 1.136 | 1.155 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑠𝑗) | 1.131 | 1.138 | 1.135 | 1.157 |

𝑀𝐼𝐷𝐴𝑆 − 𝑂𝑉𝑋 | 1.13 | 1.142 | 1.14 | 1.157 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.128 | 1.14 | 1.133 | 1.154 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑏) | 1.127 | 1.14 | 1.134 | 1.155 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑒𝑑) | 1.128 | 1.14 | 1.133 | 1.154 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(𝑚𝑖𝑛) | 1.128 | 1.14 | 1.14 | 1.155 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(−) | 1.127 | 1.141 | 1.134 | 1.156 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉(+) | 1.27 | 1.141 | 1.133 | 1.156 |

MSPE – BEIR | MSPE – MPU | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

Model | 2-Months | 4 | 6 | 8 | 10 | 2 | 4 | 6 | 8 | 10 |

𝑁𝑜𝑛 − 𝑜𝑖𝑙 | 1.1111 | 1.1453 | 1.1662 | 1.1707 | 2.2256 | 3.3384 | 12.2558 | 11.1251 | 1.1505 | 11.1329 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉 | 1.1125 | 1.1296 | 1.142 | 1.1371 | 2.2532 | 4.473 | 6.6798 | 1.111 | 12.2442 | 11.1816 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑏) | 1.1125 | 1.1293 | 1.1435 | 1.1376 | 2.2538 | 4.473 | 6.6799 | 6.6143 | 2.2423 | 11.4818 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑒𝑑) | 1.1123 | 1.1294 | 1.1435 | 1.1378 | 2.2533 | 4.473 | 6.6799 | 6.6143 | 12.2443 | 11.4831 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑚𝑖𝑛) | 1.1127 | 1.1291 | 1.1437 | 1.1184 | 2.2542 | 4.473 | 6.6799 | 6.6143 | 12.2438 | 11.4839 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(−) | 1.112 | 1.1292 | 1.1438 | 1.1376 | 2.2535 | 4.4729 | 6.6799 | 6.6143 | 12.2426 | 11.48 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(+) | 1.1122 | 1.1297 | 1.1436 | 1.1363 | 2.2548 | 4.4728 | 6.6799 | 6.6143 | 12.2462 | 11.4847 |

𝑀𝐼𝐷𝐴𝑆 − 𝑅𝑉(𝑠𝑗) | 1.1123 | 1.1305 | 1.1384 | 1.1348 | 2.2574 | 4.543 | 3.3795 | 6.6143 | 12.2468 | 11.3862 |

𝑀𝐼𝐷𝐴𝑆 − 𝑂𝑉𝑋 | 1.1112 | 1.1297 | 1.1418 | 1.1401 | 1.1574 | 4.4726 | 3.3806 | 2.21 | 2.2149 | 11.3862 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.1119 | 1.1282 | 1.1397 | 1.1328 | 1.1535 | 4.4727 | 3.379 | 2.211 | 12.244 | 11.3862 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.1122 | 1.1271 | 1.1396 | 1.1338 | 1.1548 | 4.434 | 3.3801 | 8.8102 | 12.2438 | 11.3862 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.1119 | 1.1278 | 1.14 | 1.1334 | 1.1539 | 4.4727 | 2.2806 | 8.8104 | 12.245 | 11.3862 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.1118 | 1.1275 | 1.14 | 1.1335 | 1.1547 | 4.4728 | 2.2806 | 8.8102 | 12.245 | 11.3862 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.1104 | 0.0275 | 1.1406 | 1.1336 | 1.1557 | 4.4724 | 2.2806 | 5.5102 | 12.245 | 11.3862 |

𝑀𝐼𝐷𝐴𝑆 − 𝑉𝑅𝑃 − 𝑅𝑉 | 1.111 | 1.1271 | 1.1409 | 1.1329 | --- | 4.4727 | 2.2806 | 2.9105 | --- | --- |

Model: | 2 – months | 4 – months | 5 – months | 6 – months | 10 – months |

|---|---|---|---|---|---|

core CPI (based on y – o – y changes) | |||||

𝑉𝐴𝑅 (2, 10) | 1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 |

𝐵𝑉𝐴𝑅 (2, 10) | 1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 |

IP (based on y − o − y changes) | |||||

𝑉𝐴𝑅 (2, 10) | 1.4178 | 1.8465 | 2.2024 | 2.2434 | 12.2257 |

𝐵𝑉𝐴𝑅 (2, 10) | 1.4175 | 1.8457 | 2.2997 | 2.2407 | 13.3246 |

PPI (based on y − o − y changes) | |||||

𝑉𝐴𝑅 (2, 10) | 2.6016 | 2.1774 | 4.3361 | 2.2782 | 8.8546 |

𝐵𝑉𝐴𝑅 (2, 10) | 2.6057 | 2.1831 | 4.3416 | 2.2984 | 8.8884 |

BEIR (based on y − o − y changes) | |||||

𝑉𝐴𝑅 (2, 10) | 1.1297 | 1.1376 | 1.1272 | 1.135 | 1.1896 |

𝐵𝑉𝐴𝑅 (2, 10) | 1.1288 | 1.1387 | 1.1411 | 1.1519 | 1.1551 |

MPU (based on y − o − y changes) | |||||

𝑉𝐴𝑅 (2, 10) | 4.4734 | 8.8816 | 6.6189 | 11.2658 | 12.5082 |

𝐵𝑉𝐴𝑅 (2, 10) | 4.4707 | 8.8802 | 6.6201 | 11.2687 | 12.5087 |

MSPE – Level date | MSPE – m – o – m change | MSPE – y – o – y change | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Model | 1 | 3 | 6 | 9 | 12 | 1 | 3 | 6 | 9 | 12 | 1 | 3 | 6 | 9 | 12 |

Core CPI | |||||||||||||||

VAR (5,13) | 1.1317 | 2.2656 | 1.2232 | 1.287 | 1.209 | 1.1218 | 3.3135 | 1.2584 | 1.1345 | 2.2691 | 1.1101 | 1.1390 | 1.1820 | 2.2165 | 2.2421 |

BVAR (5,13) | 1.1317 | 1.2655 | 1.2227 | 1.289 | 1.7392 | 1.128 | 2.3134 | 1.2584 | 1.1345 | 2.2691 | 1.1101 | 1.139 | 1.182 | 2.2165 | 2.2421 |

Core IPI | |||||||||||||||

𝑉𝐴𝑅 (5,13) | 1.2069 | 2.2391 | 1.1478 | 4.4081 | 15.4563 | 1.24 | 2.2385 | 2.2051 | 4.4581 | 22.323 | 1.1178 | 1.2110 | 2.2024 | 2.3434 | 14.4257 |

𝐵𝑉𝐴𝑅 (5,13) | 1.207 | 2.2592 | 1.148 | 4.4064 | 12.118 | 1.24 | 2.2379 | 2.2045 | 4.4584 | 23.322 | 1.1175 | 1.8457 | 2.2997 | 2.307 | 14.3246 |

Core PPI | |||||||||||||||

𝑉𝐴𝑅 (5,13) | 2.875 | 13.222 | 45.517 | 63.301 | 92.242 | 2.392 | 3.31 | 13.38 | 14.491 | 23.376 | 2.102 | 2.1770 | 3.236 | 3.378 | 5.4550 |

𝐵𝑉𝐴𝑅 (5,13) | 3.372 | 15.574 | 42.215 | 65.366 | 92.231 | 2.387 | 3.308 | 13.391 | 14.493 | 23.386 | 2.106 | 2.1830 | 3.242 | 3.398 | 5.4880 |

𝐵𝐸𝐼𝑅 | |||||||||||||||

VAR (5,13) | 1.116 | 1.129 | 1.144 | 1.14 | 1.1580 | ||||||||||

BVAR (5,13) | 1.113 | 1.139 | 1.147 | 1.14 | 1.1800 | ||||||||||

MPU | |||||||||||||||

𝑉𝐴𝑅 (5,13) | 4.373 | 8.882 | 6.619 | 12.266 | 12.208 | 4.491 | 11.121 | 8.44 | 13.388 | 13.339 | 12.279 | 14.439 | 13.363 | 12.288 | 12.2000 |

𝐵𝑉𝐴𝑅 (5,13) | 2.271 | 8.88 | 6.62 | 12.269 | 12.209 | 4.487 | 1.119 | 8.435 | 13.386 | 13.33 | |||||

CPI | Consumer Price Index |

IP | Industrial Production |

PPI | Producer Price Index |

U.S. | United States |

EIA | United States Energy Information Administration |

FRED | Federal Reserve Economic Data |

WTI | West Texas Intermediate |

OVX | Oil Volatility Index (WTI implied volatility index) |

MIDAS | Mixed Data Sampling |

VAR | Vector Autoregression |

BVAR | Bayesian Vector Autoregression |

OPEC | Organization of the Petroleum Exporting Countries |

GCC | Gulf Cooperation Council |

CGE | Computable General Equilibrium |

VECM | Vector Error Correction Model |

GA-NN | Genetic Algorithm-Neural Network |

WTM | Web Text Mining |

RSTM | Rough-Set-Refined Data Extraction |

RMSE | Root Mean Squared Error |

MSPE | Mean Squared Prediction Error |

MAPE | Mean Absolute Prediction Error |

MCS | Model Confidence Set |

CBOE | Chicago Board Options Exchange |

RV | Realized Volatility |

VRP | Variance Risk Premium |

BEIR | Break-Even Inflation Rate |

MPU | Monetary Policy Uncertainty |

| [1] | F. Ma, Y. Wei, W. Chen, and F. He, “Forecasting the volatility of crude oil futures using high-frequency data: further evidence,” Empir. Econ., vol. 55, no. 2, pp. 653–678, Sep. 2018, |

| [2] | U. M. Mohsin Muhammad, Dilanchiev Azer, “The Impact of Green Climate Fund Portfolio Structure on Green Finance: Empirical Evidence from EU Countries:,” Ekonomika, vol. 102, no. 2, pp. 130–144, 2023, |

| [3] | H. Yuan, L. Zhao, and M. Umair, “Crude oil security in a turbulent world: China’s geopolitical dilemmas and opportunities,” Extr. Ind. Soc., vol. 16, p. 101334, 2023, |

| [4] | Q. Wu, D. Yan, and M. Umair, “Assessing the role of competitive intelligence and practices of dynamic capabilities in business accommodation of SMEs,” Econ. Anal. Policy, vol. 77, pp. 1103–1114, 2023, |

| [5] | M. Yu, M. Umair, Y. Oskenbayev, and Z. Karabayeva, “Exploring the nexus between monetary uncertainty and volatility in global crude oil: A contemporary approach of regime-switching,” Resour. Policy, vol. 85, p. 103886, 2023, |

| [6] | F. Wen, L. Xu, G. Ouyang, and G. Kou, “Retail investor attention and stock price crash risk: evidence from China,” Int Rev Financ Anal, vol. 65, Oct. 2019, |

| [7] | C. Pierdzioch, M. Risse, and S. Rohloff, “Fluctuations of the real exchange rate, real interest rates, and the dynamics of the price of gold in a small open economy,” Empir Econ, vol. 51, no. 4, pp. 1481–1499, Dec. 2016, |

| [8] | X. CUI, M. UMAIR, G. IBRAGIMOVE GAYRATOVICH, and A. DILANCHIEV, “DO REMITTANCES MITIGATE POVERTY? AN EMPIRICAL EVIDENCE FROM 15 SELECTED ASIAN ECONOMIES,” Singapore Econ. Rev., vol. 68, no. 04, pp. 1447–1468, Apr. 2023, |

| [9] | C. Li and M. Umair, “Does green finance development goals affects renewable energy in China,” Renew. Energy, vol. 203, pp. 898–905, 2023, |

| [10] | F. Liu, M. Umair, and J. Gao, “Assessing oil price volatility co-movement with stock market volatility through quantile regression approach,” Resour. Policy, vol. 81, Mar. 2023, |

| [11] | M. Umair and A. Dilanchiev, “Economic Recovery by Developing Business Starategies: Mediating Role of Financing and Organizational Culture in Small and Medium Businesses,” Proc. B., p. 683, 2022. |

| [12] | Y. Zhang and M. Umair, “Examining the interconnectedness of green finance: an analysis of dynamic spillover effects among green bonds, renewable energy, and carbon markets,” Environ. Sci. Pollut. Res., 2023, |

| [13] | K. Gkillas, R. Gupta, and C. Pierdzioch, “Forecasting realized gold volatility: is there a role of geopolitical risks?,” Financ. Res Lett, vol. 35, Jul. 2020, |

| [14] | Y. Li and M. Umair, “The Protective Nature of Gold During Times of Oil Price Volatility: An Analysis of the COVID-19 Pandemic,” Extr. Ind. Soc., p. 101284, 2023, |

| [15] | M. Balcilar, S. Bekiros, and R. Gupta, “The role of news-based uncertainty indices in predicting oil markets: a hybrid nonparametric quantile causality method,” Empir Econ, vol. 53, no. 3, pp. 879–889, Nov. 2017, |

| [16] | X. Xiuzhen, W. Zheng, and M. Umair, “Testing the fluctuations of oil resource price volatility: A hurdle for economic recovery,” Resour. Policy, vol. 79, p. 102982, 2022, |

| [17] | T. F. M. I. A Michelis, “Oil prices and consumption across countries and U.S. States,” Int J Cent Bank, vol. 16, no. 2, pp. 3–43, 2020. |

| [18] | B. Bernanke, “Nonmonetary effects of the financial crises in the propagation of the great depression,” Am Econ Rev, vol. 73, pp. 257–276, 1983. |

| [19] | C. Baumeister, D. Korobilis, and T. K. Lee, “Energy markets and global economic conditions,” Rev Econ Stat, vol. 104, no. 4, pp. 828–844, Jul. 2020, |

| [20] | T. P. G Bampinas, “On the relationship between oil and gold before and after financial crisis: linear, nonlinear and time-varying causality testing,” Stud Nonlinear Dyn Econ., vol. 19, no. 5, pp. 657–668, 2015. |

| [21] | R. Tibshirani, “Regression shrinkage and selection via the lasso,” J R Stat Soc B, vol. 58, pp. 267–288, 1996. |

| [22] | K. Tissaoui, T. Zaghdoudi, A. Hakimi, and M. Nsaibi, “Do Gas Price and Uncertainty Indices Forecast Crude Oil Prices? Fresh Evidence Through XGBoost Modeling,” Comput. Econ., pp. 1–25, Sep. 2022, |

| [23] | H. Abdollahi, “A novel hybrid model for forecasting crude oil price based on time series decomposition,” Appl. Energy, vol. 267, p. 115035, Jun. 2020, |

| [24] | W. Ahmad, M. Aamir, U. Khalil, M. Ishaq, N. Iqbal, and M. Khan, “A new approach for forecasting crude oil prices using median ensemble empirical mode decomposition and group method of data handling,” Math. Probl. Eng., vol. 2021, 2021, |

| [25] | R. Aloui, R. Gupta, and S. M. Miller, “Uncertainty and crude oil returns,” Energy Econ., vol. 55, pp. 92–100, Mar. 2016, |

| [26] | G. A. Busari and D. H. Lim, “Crude oil price prediction: A comparison between AdaBoost-LSTM and AdaBoost-GRU for improving forecasting performance,” Comput. Chem. Eng., vol. 155, Dec. 2021, |

| [27] | M. I. Haque, “Oil price shocks and energy consumption in GCC countries: a system-GMM approach,” Environ. Dev. Sustain., vol. 23, no. 6, pp. 9336–9351, 2021. |

| [28] | P. K. Narayan and S. S. Sharma, “New evidence on oil price and firm returns,” J. Bank. Financ., vol. 35, no. 12, pp. 3253–3262, Dec. 2011. |

| [29] | N. Norouzi and M. Fani, “Black gold falls, black plague arise - An Opec crude oil price forecast using a gray prediction model,” Upstream Oil Gas Technol., vol. 5, p. 100015, Oct. 2020, |

| [30] | E. Symitsi and K. J. Chalvatzis, “The economic value of Bitcoin: A portfolio analysis of currencies, gold, oil and stocks,” Res. Int. Bus. Financ., vol. 48, pp. 97–110, Apr. 2019, |

| [31] | T. T. Azomahou, N. Ndung’u, and M. Ouédraogo, “Coping with a dual shock: The economic effects of COVID-19 and oil price crises on African economies,” Resour. Policy, vol. 72, Aug. 2021, |

| [32] | K. Koc, Ö. Ekmekcioğlu, and Z. Işık, “Developing a probabilistic decision-making model for reinforced sustainable supplier selection,” Int. J. Prod. Econ., vol. 259, no. March, 2023, |

APA Style

Ullah, I. (2025). Assessing the Role of Oil Price Forecasts in Predicting Macroeconomic Indicators: A Conditional Forecasting Approach. International Journal of Economics, Finance and Management Sciences, 13(3), 134-155. https://doi.org/10.11648/j.ijefm.20251303.16

ACS Style

Ullah, I. Assessing the Role of Oil Price Forecasts in Predicting Macroeconomic Indicators: A Conditional Forecasting Approach. Int. J. Econ. Finance Manag. Sci. 2025, 13(3), 134-155. doi: 10.11648/j.ijefm.20251303.16

@article{10.11648/j.ijefm.20251303.16,

author = {Inam Ullah},

title = {Assessing the Role of Oil Price Forecasts in Predicting Macroeconomic Indicators: A Conditional Forecasting Approach

},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {13},

number = {3},

pages = {134-155},

doi = {10.11648/j.ijefm.20251303.16},

url = {https://doi.org/10.11648/j.ijefm.20251303.16},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20251303.16},

abstract = {This research endeavor carefully examines the economic effectiveness of oil price forecasts through the lens of conditional forecasting applied to three essential macroeconomic indicators—specifically, the Consumer Price Index (CPI), Industrial Production (IP), and Producer Price Index (PPI) within the United States. The analytical framework initially adopts a mixed sampling frequency approach to identify the trajectory of oil prices, utilizing high-frequency information to enhance the predictive process. Following this, macroeconomic conditional forecasts are methodically executed. Notably, the identified trends reflect a waning importance of oil price forecasts in relation to inflation predictions. Conversely, forecasts concerning price increases, manufacturing output, and the PPI reveal an inverse correlation. The complexities underlying this phenomenon are rigorously analyzed, with multiple plausible explanations presented. The robustness of our findings is highlighted by their consistency across various model specifications and forecasting methodologies, underscoring the reliability and durability of our analytical framework. Ultimately, this research offers critical insights into the intricate relationship between oil prices and macroeconomic variables, carrying significant implications for policymakers, businesses, and investors alike. The study elucidates the nuanced dynamics of oil price forecasts and their consequential effects on macroeconomic indicators, thereby not only enhancing the comprehension of economic interdependencies but also providing practical guidance for stakeholders navigating the intricate terrain of economic forecasting. The multifaceted implications of our findings extend beyond academic circles, positioning our research as a vital resource for those responsible for crafting informed policies, strategic business decisions, and investment strategies in the continuously evolving economic landscape.

},

year = {2025}

}

TY - JOUR T1 - Assessing the Role of Oil Price Forecasts in Predicting Macroeconomic Indicators: A Conditional Forecasting Approach AU - Inam Ullah Y1 - 2025/06/30 PY - 2025 N1 - https://doi.org/10.11648/j.ijefm.20251303.16 DO - 10.11648/j.ijefm.20251303.16 T2 - International Journal of Economics, Finance and Management Sciences JF - International Journal of Economics, Finance and Management Sciences JO - International Journal of Economics, Finance and Management Sciences SP - 134 EP - 155 PB - Science Publishing Group SN - 2326-9561 UR - https://doi.org/10.11648/j.ijefm.20251303.16 AB - This research endeavor carefully examines the economic effectiveness of oil price forecasts through the lens of conditional forecasting applied to three essential macroeconomic indicators—specifically, the Consumer Price Index (CPI), Industrial Production (IP), and Producer Price Index (PPI) within the United States. The analytical framework initially adopts a mixed sampling frequency approach to identify the trajectory of oil prices, utilizing high-frequency information to enhance the predictive process. Following this, macroeconomic conditional forecasts are methodically executed. Notably, the identified trends reflect a waning importance of oil price forecasts in relation to inflation predictions. Conversely, forecasts concerning price increases, manufacturing output, and the PPI reveal an inverse correlation. The complexities underlying this phenomenon are rigorously analyzed, with multiple plausible explanations presented. The robustness of our findings is highlighted by their consistency across various model specifications and forecasting methodologies, underscoring the reliability and durability of our analytical framework. Ultimately, this research offers critical insights into the intricate relationship between oil prices and macroeconomic variables, carrying significant implications for policymakers, businesses, and investors alike. The study elucidates the nuanced dynamics of oil price forecasts and their consequential effects on macroeconomic indicators, thereby not only enhancing the comprehension of economic interdependencies but also providing practical guidance for stakeholders navigating the intricate terrain of economic forecasting. The multifaceted implications of our findings extend beyond academic circles, positioning our research as a vital resource for those responsible for crafting informed policies, strategic business decisions, and investment strategies in the continuously evolving economic landscape. VL - 13 IS - 3 ER -

Department of Economics, Allama Iqbal Open University, Islamabad, Pakistan

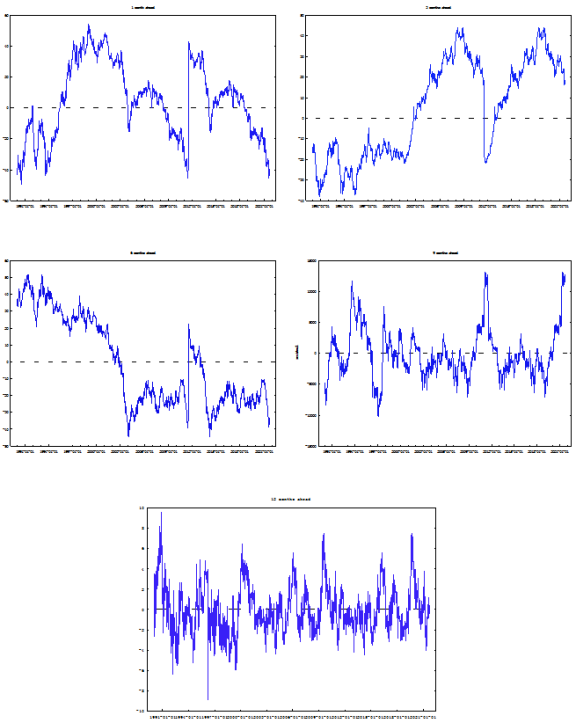

Figure 1. A pseudo-forecast oil price projection. Source: Author’s Calculation. Note: Comparison of the accuracy of oil-augmented prediction models to those without oil over 60 months.

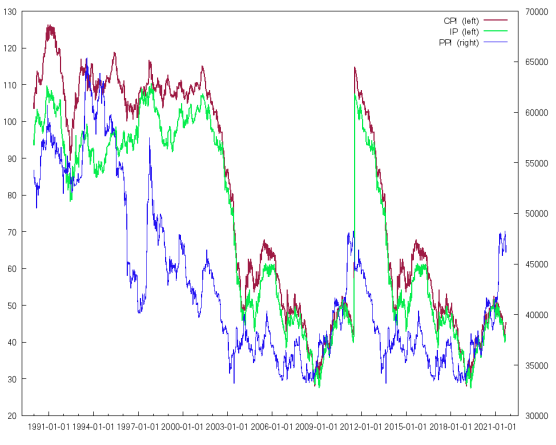

Figure 2. The core consumer price index (CPI) projections with utilizing monthly BVAR” conditional. Source: Author’s Calculation.